Don't Panic! Just Plan It.

Financial markets have been more turbulent in the past few weeks than has been seen in many years, probably more volatile than has happened since many of you started being financially aware. You may be wondering what actions you should take. With the sense of panic and urgency surrounding recent news, it often feels as if drastic action is necessary. If you have created financial plan, inaction may be the best strategy for you! If you don't have a financial plan, you might start by downloading Financial IQ by Susie Q's Personal Financial Planner.

As indicated elsewhere on this blog, I do not have any professional designations that qualify me to provide professional advice. In addition, my comments are provided as generalities and may not apply to your specific situation. Please read the rest of this post with these thoughts in mind.

Biggest Financial Risk from Recent News

I suspect that losing your job or losing business if you are self-employed is the biggest financial risk many of you face. Understanding your position within your company and how your company will be impacted by coronavirus, oil prices and other events will inform you as to the extent to which you face the risk of a lay-off or reduction in hours/salary.

If you think you might have a risk of a decrease in earned income, you’ll want to look into what options for income replacement are available to you, including state or federal unemployment programs, severance from your employers, among others. Another important step is to review your expenses so you know how you can reduce them to match your lowered income. In addition, you’ll want to evaluate how long you can live before exhausting your emergency savings, with or without drastic reductions in your expenses. You may even want to start cutting expenses before your income is lowered and put the extra amount in your emergency savings.

Your Financial Plan & Recent News

In the rest of this post, I’ll look at the various components of a financial plan and provide my thoughts on how they might be impacted by the recent news and resulting volatility in financial markets. For more tips on how to handle financial turmoil, check out these mistakes to avoid.

Paid Time-Off Benefits/Disability Insurance

If you are unfortunate enough to get COVID-19 or are required to self-quarantine and can’t work from home, you may face a reduction in compensation. Your first line of defense is any sick time or paid time-off (PTO) provided by your employer. In most cases, your employer will cover 100% of your wages for up to the number of days, assuming you haven't used them yet.Once you have used all of your sick time/PTO, you may have coverage under short- or long-term disability insurance if provided by your employer or if you purchase it through your employer or on your own. Disability insurance generally pays between 2/3 and 100% of your wages while you are unable to work for certain causes, almost always including illness. It might be a good time to review your available sick time/PTO and disability insurance to understand what coverage you have.

Emergency Savings

Emergency savings is one of the most important components of a financial plan. There are two aspects to your emergency savings that you’ll want to consider. The first is whether you have enough in your emergency savings. The second is the risk that the value of the savings will go down due to financial market issues.

Do I Have Enough?

If you are laid off, have reduced hours or use up all, exhaust your sick time/PTO or get less than 100% of your wages replaced by disability insurance, you may have to tap into your emergency savings. The need to spend your emergency savings increases if you tend to spend most of your paycheck rather than divert a portion of it to savings.

I generally suggest one to six months of expenses as a target for the amount of emergency savings. In light of recent events and the increased risks lay-off and illness, I would focus on the higher end of that range or even longer. As you evaluate the likelihood you’ll be laid off, the chances you’ll be exposed to coronavirus and your propensity to get it, you’ll also want to consider whether you have enough in emergency savings to cover your expenses while your income is reduced or eliminated.In certain situations, such as in response to the coronavirus, creditors will allow you to defer your payments. You will then have the option as to whether to defer them or make those payments from your emergency savings.

Will it Lose Its Value?

I’ve suggested that you keep at least one month of expenses in emergency savings in a checking or savings account at a bank or similar financial institution. The monetary value of your emergency savings is pretty much risk-free, at least in the US. The only way you would lose any of these savings is if the financial institution were to go bankrupt. In the US, deposits in financial institutions are insured, generally up to $250,000 per person per financial institution, by the Federal Deposit Insurance Corporation (FDIC). For more specifics, see the FDIC web site. Similar protections may be available in other countries.

I’ve also suggested that you keep another two to five months of expenses in emergency savings in something only slightly less accessible, such as a money market account. There is slightly more risk that the value of a money market account will go down than a checking or savings account, but it is generally considered to be very small. Money market accounts are also insured by the FDIC. For more specifics, see this article on Investopedia.

As such, the recent volatility in financial markets are unlikely to require you to take action related to your existing emergency savings and could act as an opportunity to re-evaluate whether you have enough set aside for emergencies.

Short-Term Savings

Another component of a financial plan is short-term savings. Short-term savings is money you set aside for a specific purpose. One purpose for short-term savings is expenses that don’t get paid every month, such as property taxes, homeowners insurance or car maintenance and repairs. Another purpose for short-term savings is to cover the cost of larger purchases for which you might need to save for several years, such as a car or a down payment on a house.

Short-term savings are commonly held in money-market accounts, certificates of deposits (CDs) or very high quality, shorter term bonds, such as those issued by the US government. CDs and US government bonds held to maturity are generally considered to have very little risk. Their market values are unlikely to change much and the likelihood that the issuers will not re-pay the principal when due is small.

Thus, the recent volatility in financial markets is also unlikely to require you to take action related to your short-term savings.

Long-Term Savings

Savings for retirement and other long-term goals are key components of a financial plan. If they are invested at all in any equity markets, your long-term savings have likely taken quite a beating. Rather than try to provide generic guidance on how to deal with the losses in your long-term savings, I’ll tell you how I’m thinking and what I’m doing about mine. By providing a concrete example, albeit one very different from most of your situations, my goal is to provide you with some valuable insights about the thought process.

Think about the Time Frame for My Long-Term Savings

As you may know, I’m retired and have just a little income from consulting. As such, my financial plan anticipates that I will live primarily off my investments and their returns. I have enough cash and bonds to cover my expenses for several years. As such, I’m not in a position that I absolutely have to liquidate any of my equity positions in less than three-to-four years.

For many of you, your most significant goal for long-term savings is likely retirement. As such, your time horizon for your long-term savings is longer than mine and you can withstand even more volatility. That is, you have a longer time for stock prices to recover to the recent highs and even higher.

In the final section of this post, I’ll talk about how long it has taken equity markets to recover from past “crashes” to help you get more perspective on this issue.

Know Your Investments

My view is that, if I wait long enough, the overall stock market will recover. It always has in the past. If it doesn’t, I suspect something cataclysmic will have happened and I will be focused on more important issues such as food, water and heat, than my long-term savings. For now, though, my view is that my investments in broad-based index funds are going to recover from the recent price drops though it may take a while and be a tough period until then. As such, I am not taking any action with respect to those securities. Once the stock market seems to settle down a bit (and possibly not until it starts going up for a while), I might invest a bit more of my cash to take advantage of the lower prices.

I have a handful of investments in stocks and bonds of individual companies. These positions have required a bit more thought on my part. I already know the primary products and services of these companies and the key factors that drive profitability, as I identified these features before I purchased the stocks or bonds as part of my financial plan. I can now look at the forces driving the economic changes to evaluate how each of the companies might be impacted.

Example 1

I own some bonds that mature in two to three years in a large company that provides cellular phone service. As discussed in my post on bonds, as long as you hold bonds to maturity, the only risk you face is that the issuer will default (not make interest payments or re-pay the principal). With the reduction in travel and group meetings, I see an increased demand for technological communication solutions, such as cell phones. While the stock price of this company has gone down, I don’t see that its chance of going bankrupt has been affected adversely, so don’t plan to sell the bonds.

Example 2

One company whose stock I’ve owned for a very long time focuses on products used to test food safety. While the company’s stock price has dropped along with the broader market, I anticipate that people will have heightened awareness of all forms of ways of transmitting illness, including through food-borne bacteria and other pathogens. As such, I am not planning to sell this stock as the result of recent events.

Example 3

I own stock in an airline that operates primarily within North America. This one is a bit trickier. It looks like travel of all types is going to be down for a while. I’m sure that US domestic airline travel will be significantly impacted, but suspect it will not be affected as much as international or cruise ship travel. The reduction in revenue might be slightly offset by the lower cost of fuel, but that is probably not a huge benefit in the long term.

I’ve owned this company for so long that I still have a large capital gain and would have to pay tax on it if I sold the stock. At this point, I don’t think there is a high probability that this airline will go bankrupt (though I’m not an expert and could be wrong). I expect the price to drop more than the overall market average in the coming months, but also expect that it will recover. As such, I don’t plan to sell this stock solely because of recent events. However, if this company had most of its revenue from operating cruise ships, was smaller, or had more foreign exposure, I would study its financials and business model in more detail to see if I thought it would be able to withstand the possibility of much lower demand for an extended period of time.

Summary

I have gone through similar thought processes for each of the companies in my portfolio to create my action plan. I will re-evaluate them as time passes and more information becomes available. If my advice isn't enough, consider Warren Buffett's evaluation of his individual stock positions, as described by Kat Rucker.

What We Can Learn from Past Crashes

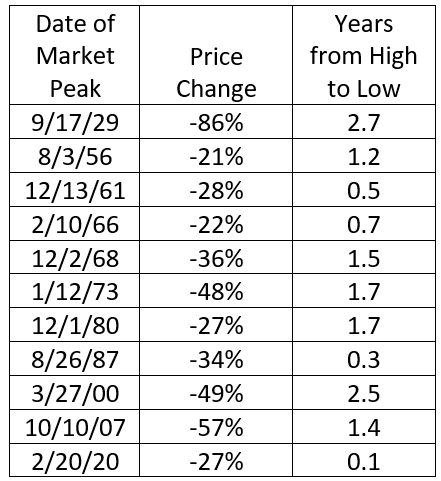

Although every market cycle is different, I thought it might be insightful to provide information about previous market crashes. For this discussion, I am defining a market crash as a decrease in the price of the S&P 500 by more than 20% from its then most recent peak. I have identified 11 crashes using this definition, including the current one, over the time period from 1927 to March 14, 2020.

As you’ll see in the graphs below, the market crash starting at the peak in August 1929 is much different from most of the others. It took until 1956 before the S&P 500 reached its pre-crash level! Over the almost three years until the S&P 500 reached its low and then again during the recovery period (from the low until it reached its previous high), there were several crashes. I have counted this long cycle as a single crash, though it could be separated into several.

Magnitude of Previous Crashes

The table below shows the dates of the highest price of the S&P 500 before each of the 11 crashes since 1927. It also shows the percentage decrease from the high to the low and the number of years from the high to the low.

While they don’t happen all that often, this table confirms that the S&P 500 has suffered significant decreases in the past. What seems a bit different about the current crash is the speed at which prices have dropped from the market high reached just a few weeks ago. In the past, the average time from the market peak to the market bottom has been 1.4 years, but the range has been from 0.3 years to 2.7 years. While the 27% decrease in the S&P 500 from its peak on February 20, 2020 until March 14, 2020 is large and troubling, the average price change of 10 preceding crashes is -41% (-36% if the 1929 crash is excluded). As such, it isn’t unprecedented.

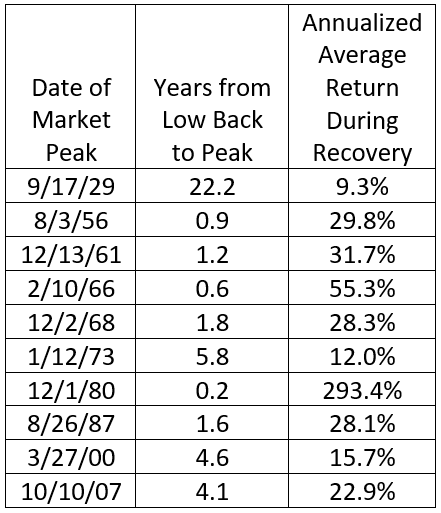

What Happened Next?

This table shows how long it took after each of the first 10 crashes for the S&P 500 to return to its previous peak. It also shows the average annualized return from the lowest price until it returned to its previous peak.

For example, it took 1.6 years after the market low price on December 4, 1987 (the low point of the cycle starting on August 26, 1987) for the S&P 500 to reach the same price it had on August 26, 1987. Over that 1.6-year period, the average annual return on an investment in the S&P 500 would have been 28%!

Because the values from the 1929 and 1980 cycles can distort the averages, I'll look at the median values of these metrics. At the median, it took 1.7 years for the S&P 500 to reach its previous high with a median annualized average return of 28%. There are obviously wide ranges about these metrics, but, excluding the 1929 crash, the S&P 500 never took more than 6 years to recover from its low. This time frame is important as you are thinking about the length of time until you might need to use your long-term savings.

After hitting bottom, the S&P 500 always had an average annual return of 12% or more over the recovery period, a fair amount higher than the overall annual average return on the S&P 500. Anyone who sold a position in the S&P 500 at any of the low points missed the opportunity to earn these higher-than-average returns - a reminder to not panic.

From Crash to Recovery

The graph below shows the ratios of the price of the S&P 500 to the price at the peak (day 0) over the 30 years after each of the first 10 market peaks in the tables above.

The light blue line that stays at the bottom is the 1929 crash. As you can see, by 30 years later, the S&P 500 was only twice as high as it was at its pre-crash peak. For all of the other crashes, the S&P 500 was at least four times higher than at each pre-crash peak, even though in many cases there were subsequent crashes in the 30-year period.

To get a sense for how the current crash compares, the graph below shows the same information for only the first 100 days after each peak.

The current crash is represented by the heavy red line.As indicated above, one of the unique characteristics about the current crash is that it occurred so quickly after the peak. The graph shows that the bright red line is much lower than any of the other lines on day 17. However, if you look at the light blue line (after the peak on September 17, 1929) and the brown line (after the peak on August 26, 1987), you can see that there were similarly rapid price decreases as occurred in the current crash, but they started a bit longer after their respective peaks.

Current Crash

We can’t know the path that the stock market will take going forward in the current cycle. It could halt its downward trend in a few days to a week and return to set new highs later this year. On the other hand, if other events occur in the future (such as the weather conditions that led to the dust bowl in the 1930s and World War II in the 1940s that exacerbated the banking issues that triggered the 1929 crash), it is possible stock prices could decline for many years and take a long time to recovery. Based on the patterns observed, this trend is less likely, but it is still a possibility.

As such, it is important as you consider your situation that you look at your investment horizon, your ability to live with further decreases in stock prices and your willingness to forego the opportunity to earn higher-than-average returns when the stock market returns to its pre-crash levels if you sell now, among other things.

Closing Thoughts

My goal in writing this post was to provide you with insights on how to view the disruptions in the economy and financial markets in recent weeks and plan your responses to them. My primary messages are:

Don’t panic. While significant action may be the best course for your situation, do your best to make well-reasoned and not emotional decisions. Although you might want to sell your investments right away to avoid additional decreases in value, it isn’t the best strategy for everyone.

Stick with (or make) a financial plan. Having a financial plan provides you with the ability to look at the impact of the uncertainties in financial markets and the overall economy on each aspect of your financial future separately, making the decision-making process a little easier.